Glossary ! - Investment & Mutual Funds !

Mutual Fund—An investment company that buys a portfolio of securities selected by a professional investment adviser to meet a specified financial goal. Mutual fund investors buy shares in the fund that represent ownership in all the fund’s securities. A mutual fund stands ready to buy back its shares at their current net asset value, which is the total market value of the fund’s investment portfolio, minus its liabilities, divided by the number of shares outstanding. Most mutual funds continuously offer new shares to investors.

Annual and Semiannual Reports— Summaries that a mutual fund sends to its

shareholders that discuss the fund’s performance over a certain period and identify the

securities in the fund’s portfolio on a specific date.

Appreciation—An increase in an investment’s value.

Asked or Offering Price—(As seen in some mutual fund newspaper listings, see p. 32.)

The price at which a mutual fund’s shares can be purchased. The asked or offering

price includes the current net asset value per share plus any sales charge.

Assets—The current dollar value of the pool of money shareholders have invested in

a fund.

Automatic Reinvestment—A fund service giving shareholders the option to purchase

additional shares using dividends and capital gains distributions.

Average Portfolio Maturity—The average maturity of all the bonds in a bond fund’s

portfolio.

Bear Market—A period during which security prices in a particular market (such as

the stock market) are generally falling.

Bid or Sell Price—The price at which a mutual fund’s shares are redeemed, or

bought back, by the fund. The bid or redemption price is usually the current net

asset value per share.

Bond—A debt security, or IOU, issued by a company, municipality, or government

agency. A bond investor lends money to the issuer and, in exchange, the issuer promises

to repay the loan amount on a specified maturity date; the issuer usually pays the

bondholder periodic interest payments over the life of the loan.

Broker/Dealer (or Dealer )—A firm that buys and sells mutual fund shares and other

securities from and to investors.

Bull Market—A period during which security prices in a particular market (such as

the stock market) are generally rising.

Capital Gains Distribution—Profits distributed to shareholders resulting from the

sale of securities held in the fund’s portfolio.

Closed-end Fund—A type of investment company that has a fixed number of shares

which are publicly traded. The price of a closed-end fund share fluctuates based on

investor supply and demand. Closed-end funds are not required to redeem shares and

have managed portfolios.

Commission—A fee paid by an investor to a broker or other sales agent for investment

advice and assistance.

Compounding—Earnings on an investment’s earnings. Over time, compounding

can produce significant growth in the value of an investment.

Contingent Deferred Sales Charge (CDSC)—A fee imposed when shares are

redeemed (sold back to the fund) during the first few years of ownership.

Credit Risk—The possibility that a bond issuer may not be able to pay interest and

repay its debt.

Custodian—An organization, usually a bank, that holds the securities and other

assets of a mutual fund.

Depreciation—A decline in an investment’s value.

Diversification—The practice of investing broadly across a number of securities to

reduce risk.

Dollar -cost Averaging—The practice of investing a fixed amount of money at regular

intervals, regardless of whether the securities markets are declining or rising.

Exchange Privilege—A fund option enabling shareholders to transfer their

investments from one fund to another within the same fund family as their needs or

objectives change. Typically, fund companies allow exchanges several times a year for a

low or no fee.

Expense Ratio—A fund’s cost of doing business—disclosed in the prospectus—

expressed as a percent of its assets.

Face Value—The amount that a bond’s issuer must repay at the maturity date.

Family of Funds—A group of mutual funds, each typically with its own investment

objective, managed and distributed by the same company.

401(k) Plan—An employer-sponsored retirement plan that enables employees to

make tax-deferred contributions from their salaries to the plan.

403(b) Plan—An employer-sponsored retirement plan that enables employees of

universities, public schools, and non-profit organizations to make tax-deferred contributions

from their salaries to the plan.

457 Plan—An employer-sponsored retirement plan that enables employees of state

and local governments and other tax-exempt employers to make tax-deferred contributions

from their salaries to the plan.

Hedge Fund—A private investment pool for wealthy investors that, unlike a mutual

fund, is exempt from SEC regulation.

Income—Dividends, interest and/or shortterm capital gains paid to a mutual fund’s

shareholders. Income is earned on a fund’s investment portfolio after deducting operating

expenses.

Individual Retirement Account (IRA)— An investor-established, tax-deferred

account set up to hold and invest funds until retirement.

Inflation Risk—The risk that a portion of an investment’s return may be eliminated by

inflation.

Interest Rate Risk—The possibility that a bond’s or bond mutual fund’s value will

decrease due to rising interest rates.

Investment Adviser—An organization employed by a mutual fund to give professional

advice on the fund’s investments and asset management practices.

Investment Company—A corporation, trust, or partnership that invests pooled

shareholder dollars in securities appropriate to the organization’s objective. Mutual

funds, closed-end funds, and unit investment trusts are the three types of investment

companies.

Investment Objective—The goal that an investor and mutual fund pursue together (e.g., current income, long-term capital growth, etc.).

Issuer—The company, municipality, or government agency that issues a security, such as a stock, bond, or money market security.

Large-cap Stocks—Stocks of large-capitalization companies, which are generally considered

to be companies whose total outstanding shares are valued at $10 billion or more.

closed-end fund is an investment company whose shares are publicly traded like stocks. As a result, the price of a closed-end fund share fluctuates based on supply and demand. If the share price is more than the value of its assets, then the fund is trading at a premium; if the share price is less, then it is trading at a discount. The assets of a closed-end fund are managed by a professional or a group of professionals choosing investments such as stocks and bonds to match the fund’s objectives.

unit investment trust (UIT) is an investment company that buys a fixed portfolio of stocks or bonds. A UIT holds its securities until the trust’s termination date. When a trust is dissolved, proceeds from the securities are paid to shareholders. UITs have a fixed number of shares or “units” that are sold to investors in an initial public offering. If some shareholders redeem units, the UIT or its sponsor may purchase them and reoffer them to the public.

Net Asset Value (NAV)—The per-share value of a mutual fund, found by subtracting the fund’s liabilities from its assets and dividing by the number of shares outstanding.Mutual funds calculate their NAVs at least once daily.

No-load Fund—A mutual fund whose shares are sold without a sales commission and without a 12b-1 fee of more than .25 percent per year.

Open-end Investment Company—The legal name for a mutual fund, indicating that it stands ready to redeem (buy back) its shares from investors on any business day.

Operating Expenses—Business costs paid from a fund’s assets before earnings are distributed to shareholders. These include management fees and 12b-1 fees and other expenses.

Portfolio—A collection of securities owned by an individual or an institution (such as a mutual fund) that may include stocks, bonds, and money market securities.

Portfolio Turnover—A measure of the trading activity in a fund’s investment portfolio—

how often securities are bought and sold by a fund.

Prepayment Risk—The possibility that a bond owner will receive his or her principal investment back from the issuer prior to the bond’s maturity date.

Portfolio Turnover—A measure of the trading activity in a fund’s investment portfolio—

how often securities are bought and sold by a fund.

Liquidity—The ability to readily access invested money. Mutual funds are liquid because their shares can be redeemed for current value (which may be more or less than the original cost) on any business day.

Long-term Funds—A mutual fund industry designation for all funds other than money market funds. Long-term funds are broadly divided into equity (stock), bond, and hybrid funds.

Management Fee—The amount paid by a mutual fund to the investment adviser for its services.

Maturity—The date by which an issuer promises to repay the bond’s face value.

Prepayment Risk—The possibility that a bond owner will receive his or her principal investment back from the issuer prior to the bond’s maturity date.

Prospectus—The official document that describes a mutual fund to prospective investors. The prospectus contains information required by the SEC, such as investment objectives and policies, risks, services, and fees.

Quality—The creditworthiness of a bond issuer, which indicates the likelihood that it will be able to repay its debt.

Redeem—To cash in mutual fund shares by selling them back to the fund. Mutual fund shares may be redeemed on any business day. You will receive the current share price, called net asset value, minus any deferred sales charge or redemption fee.

Reinvestment Privilege—An option whereby mutual fund dividends and capital gains distributions automatically buy new fund shares.

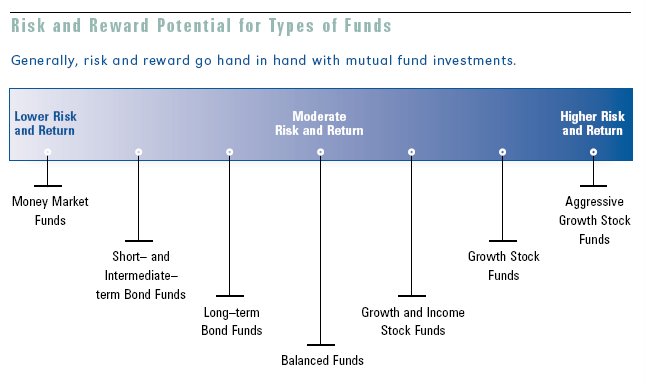

Risk/Reward Tradeoff—The investment principle that an investment must offer higher potential returns as compensation for the likelihood of increased volatility.

Rollover—The shifting of an investor’s assets from one qualified retirement plan to another—due to changing jobs, for instance—without a tax penalty.

Sales Charge or Load—An amount charged for the sale of some fund shares, usually those sold by brokers or other sales professionals. By regulation, a mutual fund sales charge may not exceed 8.5 percent of an investment purchase. The charge may vary depending on the amount invested and the fund chosen. A sales charge or load is reflected in the asked or offering price

Series Fund—A group of different mutual funds, each with its own investment objective

and policies, that is structured as a single corporation or business trust.

Share Classes (e.g., Class A , Class B,etc.)—Represent ownership in the same fund, but charge different fees. This can enable shareholders to choose the type of fee structure that best suits their particular needs.

Shareholder—An investor who owns shares of a mutual fund or other company.

Short-term Funds—Another term for money market funds.

Small-cap Stocks—Stock of smallcapitalization companies, which are generally considered to be companies whose total outstanding shares are valued at less than $1.6 billion.

Spread—The difference between what you pay for a stock or bond and what the security dealer pays for it.

Statement of Additional Information (SAI) —The supplementary document to a

prospectus that contains more detailed information about a mutual fund; also known as “Part B” of the prospectus.

Stock—A share of ownership or equity in a corporation.

Total Return—A measure of a fund’s performance that encompasses all elements of

return: dividends, capital gains distributions, and changes in net asset value. Total

return is the change in value of an investment over a given period, assuming reinvestment

of any dividends and capital gains distributions, expressed as a percentage of the

initial investment.

Transfer Agent —The organization employed by a mutual fund to prepare and

maintain records relating to shareholder accounts.

12b-1 Fee—A mutual fund fee, named for the SEC rule that permits it, used to pay for

broker-dealer compensation and other distribution costs. If a fund has a 12b-1 fee, it

will be disclosed in the fee table of a fund’s prospectus.

Underwriter —The organization that sells a mutual fund’s shares to broker/dealers and investors.

Unit Investment Trust (UIT)—An investment company that buys and holds a fixed

number of shares until the trust’s termination date. When the trust is dissolved, proceeds

are paid to shareholders. A UIT has an unmanaged portfolio. Like a mutual

fund, shares of a UIT can be redeemed on any business day.

Withdrawal Plan —A fund service allowing shareholders to receive income or principal

payments from their fund account at regular intervals.

Yield —A measure of net income (dividends and interest) earned by the securities in the

fund’s portfolio less fund expenses during a specified period. A fund’s yield is expressed

as a percentage of the maximum offering price per share on a specified date.

posted by Ashish Khandelwal @ 11:41 PM

1 comments

![]()